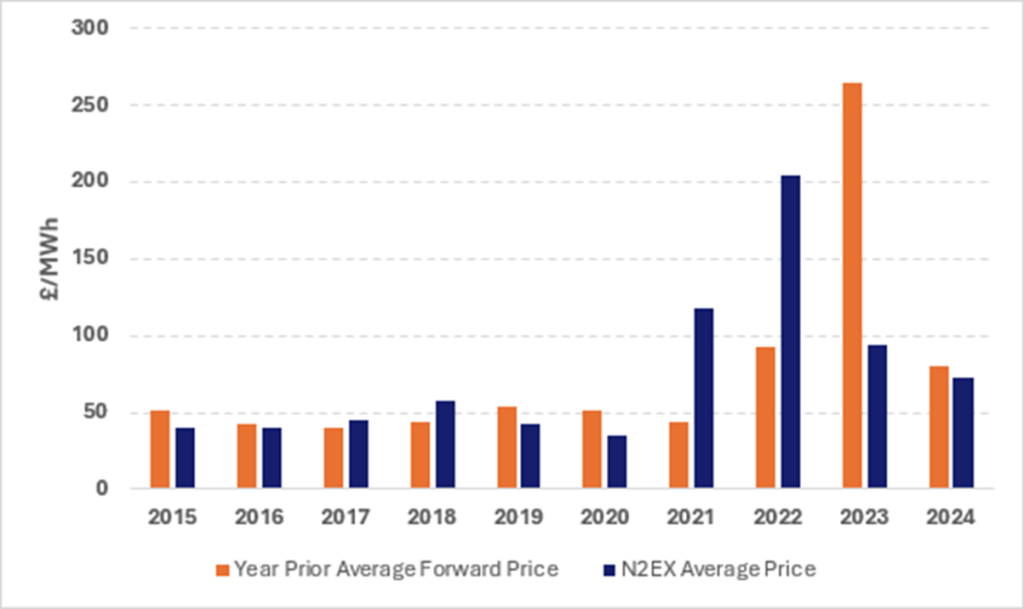

High commercial energy costs continue to place sustained pressure on UK businesses. While wholesale prices have eased since their peak, electricity and gas costs remain well above pre-2022 levels. For energy-intensive sectors, this is not a short-term headache but a structural challenge demanding new ways of thinking about energy use.

Few sectors feel this more keenly than cold storage. Between 2021 and 2022, electricity prices for many operators doubled almost overnight. The result has been an urgent drive to improve energy efficiency, reduce carbon emissions, and protect already tight margins, often while relying on ageing infrastructure and operating within strict temperature and compliance requirements.

Yet hidden within this challenge is an opportunity. Under the right conditions, cold store equipment, from compressors and refrigeration packs to ice banks, thermal stores, heat pumps, and glycol chillers, can be transformed from pure cost centres into revenue-generating assets. The key lies not in major capital investment, but in smarter control of when these assets consume power.

Why the grid needs flexibility

Traditionally, electricity systems have worked on a simple principle: generation follows demand. Power stations ramp up and down to match how much electricity consumers happen to be using at any given moment.

As the UK transitions to a low-carbon energy system, that model is under strain. Renewable generation is inherently variable; you cannot instruct the wind to blow or the sun to shine on cue. With less control over supply, the system operator increasingly needs flexibility from the demand side.

This is known as consumer-led flexibility. According to the National Energy System Operator, Britain currently has around 2.5GW of consumer-led flexibility capacity. By 2030, that figure needs to rise to 10 12GW to maintain grid stability and security. For businesses willing to participate, this represents a significant commercial opportunity.

How cold storage facilities can respond

Any asset that can briefly pause consumption, sometimes for only a few minutes, or shift its operation slightly earlier or later than planned, can provide valuable flexibility to the grid. Cold storage facilities are particularly well-suited to this role.

Compressors and related systems can be modulated in response to real-time grid conditions, ambient temperature, and site demand, without risking product integrity or regulatory compliance. Crucially, operators remain in control: participation is voluntary, parameters are agreed in advance, and everyday operations are not disrupted.

During periods of grid stress, facilities can be paid to temporarily reduce consumption. At times of surplus renewable generation, they may also be rewarded for increasing demand. Over the course of a year, depending on asset size and participation levels, many cold stores can generate several thousand pounds in additional revenue.

End to end flexibility services such as FlexGO by Flexitricity identify suitable assets, install the necessary controls and manage participation in flexibility markets, from dispatch through to settlement and payment. This allows site teams to stay focused on operations while their equipment works harder financially.

High energy prices are unlikely to disappear altogether. Grid flexibility offers cold storage operators a practical way to offset costs, reduce carbon impact and unlock new value from existing infrastructure.

How Growers Can Earn Revenue Through Flexible Operation

Energy pressures are not confined to cold storage. Across the UK, growing, rising electricity and gas costs are pushing some growers to the brink. In a recent letter to Ofgem, the National Farmers’ Union warned that energy prices are threatening the viability of many farmers’ and growers’ businesses.

For growers operating controlled environments year-round, energy is typically the second-highest cost after labour. LED lighting, combined heat and power (CHP), heat pumps, water pumps, and refrigeration are essential to maintaining crop quality, but they are also energy hungry.

As with cold storage, these assets can do more than simply consume electricity. With the right controls in place, they can also generate income by supporting the electricity grid.

Flexibility in practice for growers

The principle is straightforward. Any equipment that can pause, ramp down, or shift consumption without affecting output can provide flexibility. For growers, this may include dimming or rescheduling LED lighting, adjusting CHP operation, or briefly delaying non-critical pumping and refrigeration cycles.

Participation does not mean relinquishing control. Growers decide when and how their assets are made available, ensuring crop conditions and yields are never compromised. Flexibility events are typically short and carefully managed.

Depending on the scale of the site and the number of assets enrolled, many growers can earn several thousand pounds a year, an income that directly offsets energy bills while contributing to a more resilient, low-carbon grid.

Providers such as FlexGO by Flexitricity deliver a fully managed service, from asset assessment and installation through to market participation and payment administration. This allows growers to focus on production while turning unavoidable energy use into a strategic advantage.

A new role for energy-intensive businesses

For both cold storage operators and growers, flexibility represents a shift in mindset. Energy is no longer just a cost to be minimised, but a resource that can be optimised, traded and monetised.

As the UK’s electricity system continues to decarbonise, the value of flexible demand will only grow. Those who act early stand to benefit, financially and environmentally, without disrupting the day-to-day realities of running complex, energy-dependent operations.

This article appeared in the Jan/Feb 2026 issue of Energy Manager magazine. Subscribe here.

")