For industrial and commercial (I&C) energy consumers, procurement has long been driven by a single overriding objective: price certainty. Fixed-price contracts, long-term supply agreements, and Power Purchase Agreements (PPAs) have been the default tools for managing exposure to wholesale power markets. They deliver predictability, can align with sustainability targets, and provide comfort in periods of rising prices.

Yet certainty alone does not equal value.

As power markets evolve, it is becoming increasingly clear that strategies built solely around long-term price fixing struggle to deliver optimal outcomes over time. In an environment defined by renewable-driven volatility, sharper intraday price swings, and frequent structural change, energy procurement must now balance cost protection and cost efficiency – not trade one for the other.

Why traditional hedging leaves value on the table

Long-term fixed pricing plays an important role in energy risk management, but it has a structural weakness: if markets fall, consumers are locked in at their fixed price and fail to benefit from lower prices.

That cost takes several forms:

- Embedded risk premiums within fixed prices

- Trading and structuring fees that are often opaque

- Opportunity loss when wholesale prices fall below the fixed level

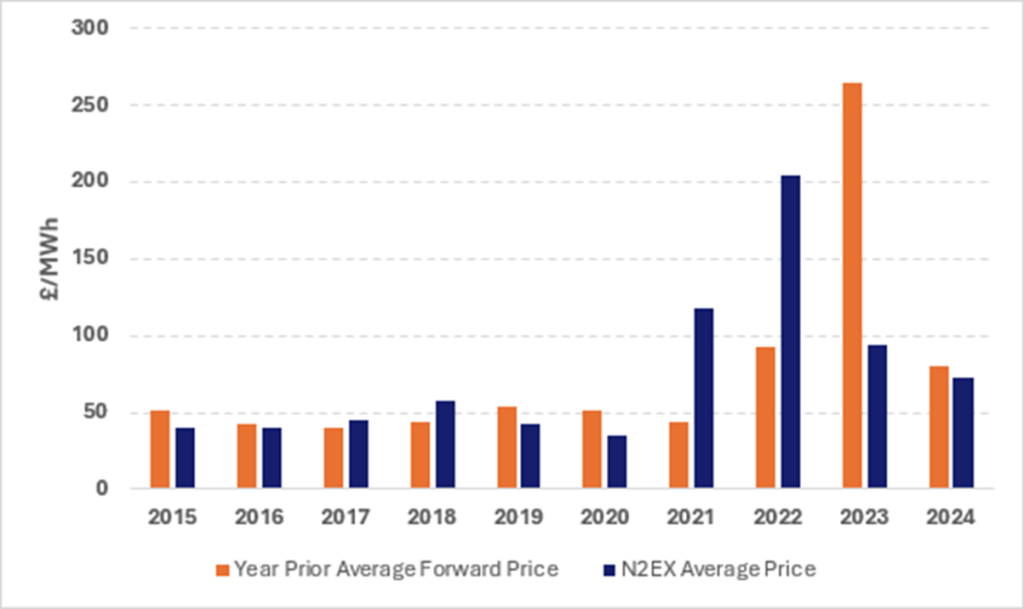

Over the past decade, wholesale electricity prices have repeatedly undershot forward market expectations. In those periods, consumers locked into fixed pricing paid materially more than the realised cost of energy. While this underperformance may not be visible in any single year, it becomes increasingly pronounced when assessed over longer time horizons.

Put simply, price certainty does not guarantee cost minimisation.

A broader toolkit for modern energy buyers

Power markets today offer more than a binary choice between fixed and floating prices. Increased liquidity, better data, and a growing ecosystem of financial risk-transfer solutions have expanded what is possible for sophisticated buyers.

Most procurement approaches still fall into one of three categories:

- Fixed pricing. Locking in prices offers protection against adverse market movements and simplifies budgeting. However, when prices trend lower or fall sharply, organisations remain committed to above-market costs, often for years.

- Floating pricing. Index-linked procurement allows organisations to fully benefit from falling prices and avoids embedded premiums. The trade-off is exposure to extreme price events, which can severely disrupt budgets and cash flow.

- Hybrid models. Blended strategies aim to balance these risks but typically require active management, frequent rebalancing, and ongoing market engagement. Each adjustment introduces frictional costs and operational complexity.

While each approach has merit, none fully resolves the tension between protecting budgets and capturing market opportunity.

Separating risk protection from energy purchasing

An alternative framework is one that separates price risk management from physical energy procurement.

Rather than embedding risk protection inside energy supply contracts, this approach uses external, AA-rated insurance to cap exposure to extreme price events. Energy itself continues to be purchased at market-linked rates through an existing supplier, ensuring full participation when prices fall.

Key characteristics include:

- Protection against upward price spikes through insurance

- Direct benefit from lower wholesale prices when markets soften

- No requirement to change supplier or restructure supply contracts

- Clearly defined cost ceilings aligned with internal risk limits

Because risk is priced explicitly rather than embedded within energy rates, this model improves transparency and avoids many of the hidden costs associated with fixed-price contracts.

Solutions such as the Paratus structure, backed by Lloyd’s of London, are designed specifically to operate alongside standard utility supply agreements, offering a practical path to more efficient risk management.

What the data shows

Using UK power price data from 2014 to 2024 (sourced from Bloomberg), a comparative analysis was conducted across three procurement strategies:

- Annual forward price fixing

- Full exposure to realised market prices

- Market exposure combined with insured price protection

Over the ten-year period, the insured market-exposure approach delivered more than £10/MWh in cumulative savings relative to fixed-price hedging after accounting for the full cost of the insurance.

For a 100,000 MWh annual portfolio, that equates to over £1 million per year in value, without increasing exposure to extreme price events.

A shift in procurement thinking

The implication is not that fixed pricing or PPAs should be abandoned. Rather, they should be viewed as components of a broader strategy – not the strategy itself.

As markets become harder to predict, resilience comes from flexibility. Procurement models that allow participation in favourable market outcomes, while retaining protection against tail risks, are structurally better suited to today’s energy landscape.

The era of one-way energy procurement is ending. The future belongs to strategies that recognise uncertainty and are designed to perform because of it, not in spite of it.

In modern power markets, managing energy costs is no longer about choosing between certainty and opportunity. With the right tools, organisations can, and increasingly must, achieve both.

This article appeared in the Jan/Feb 2026 issue of Energy Manager magazine. Subscribe here.